The bankruptcy of large crypto companies opened the way for new players in the market

This year, however, like many past years, was rich in events, news and price movements. The global capital market began it against the backdrop of record performance in the value of shares and cryptocurrencies and a post-Covid reassessment of the prospects of many sectors, including technology companies.

The discussion among experts about the prospects for the American and global economy, which began at the end of 2021, began to develop more and more actively by the beginning of spring. Macro statistics, data on unemployment, the cost of resources, components and logistics caused increasing concern about the market outlook. As a result, high persistent global inflation has become a fact that cannot be ignored. The financial authorities of the world’s largest economies began the process of raising rates, however, different countries had different dynamics and expectations regarding the final effect of these processes. And so the high correlation between the largest equity markets, including cryptocurrencies, has been replaced by turbulence and fragmentation of cash flows.

Since May, local factors have become increasingly important in each of the markets. The pace of rate hikes in the US was faster than other markets and began to outpace the rate of inflation decline. The strengthening of the dollar index was replaced by a decline towards the end of the year. European and Asian markets began to show stronger dynamics in anticipation of the onset of affordable and loyal financing conditions. In this situation, the crypto market was left to itself – large trading liquidity left the niche market as part of the risk reduction and global diversification regime.

Rate hike

At the moment, the refinancing rate in the key US market is close to the maximum values in recent years and is 4-4.25%. However, further prospects regarding the maximum level of tightening are contradictory. As practice has shown, the Fed is late in reacting to changing market conditions, and following the results of the last meeting, it issued a statement that they do not intend to reduce the rate in 2023. However, stock traders have a different opinion and expect the decline to begin in the fall of 2023. This parameter is extremely important for cryptocurrencies, since the last cycle of low rates and cheap liquidity was one of the main reasons for last year’s price records.

General Crypto market cap

Since the beginning of the year, the capitalization of the crypto market has fallen almost three times – from a peak of 2.25 trillion to 780 billion at the end of the year. The market went through a series of shocks in a short time. The collapse of the ecosystem of the entire LUNA blockchain in May and the subsequent bankruptcy of large hybrid CeDeFi crypto-landers ended in an epoch-making bankruptcy of one of the largest exchanges, FTX.

Such events force us to re-evaluate the meaning of the concepts of “reliability” and “decentralization”. However, it is completely decentralized protocols (such as AAVE and Maker) that have shown that they can withstand stress tests as intended, and passing this “obstacle course” only emphasizes their merits as an alternative to future finance.

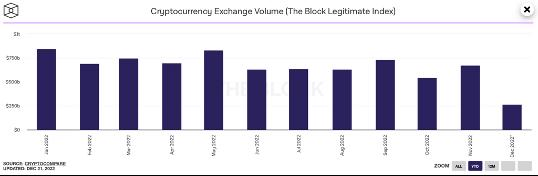

Spot market

The volume of trading on the spot market decreased following the fall in the rate of cryptocurrencies. From a peak of over 800 billion in January to just under 600 billion in November. The trend strengthened in early autumn and peaked in November after FTX fell.

At the same time, the three largest exchanges Coinbase, Kraken and Binance (among exchanges that directly accept deposits in fiat currencies) benefited from this event. In general, the decrease in trading volume is quite expected and not critical for the industry, which can potentially only affect the valuation of public companies.

With far more serious long-term consequences, another emerging trend is the stablecoin ecosystem war. Competition in the market in the face of a decline in liquidity has increased significantly, which has led to the search for new advantages between trading ecosystems. Stablecoins have taken the place of an understandable first gate for a new user to enter the industry. The logic of retaining current and attracting new users forced Binance to remove the second USDC stable by capitalization from the quotes, leaving the opportunity to trade cryptocurrencies only with BUSD and USDT. Such actions were not slow to affect the issue volume, which for BUSD increased from 14 billion in the spring of 2022 to 22 billion in November. USDT remains the most popular stablecoin, but in the future, the presence of different stablecoins in blockchains will be much more important in the fight for the end user.

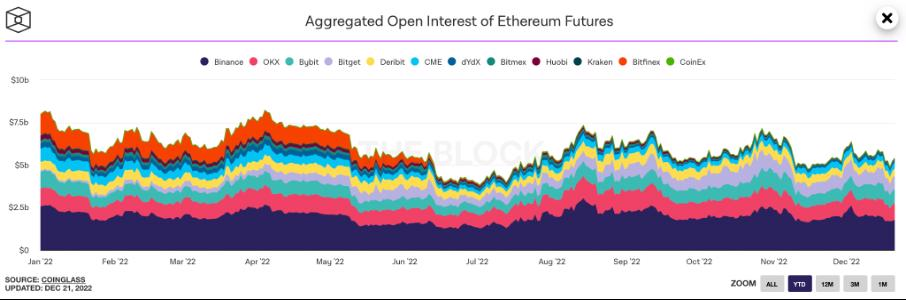

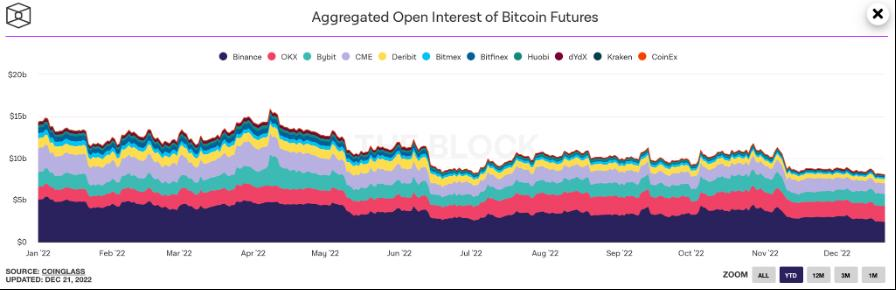

Futures

Futures trading volume also declined, but in different ways for Bitcoin and Ethereum. If for the first cryptocurrency at the beginning of the year 13-15 billion were standard, then by the end of the year this figure had halved to 7.5 billion. For ether, similar metrics started at 7.5 billion with a downward trend. However, the change in the consensus algorithm to proof-of-stake has spurred interest in ETH. As a result of a small summer local bull run, there was even a small gamma squeeze on options. As a result, the current volume of open interest has stabilized at the level of 5.5 billion with some upward trend.

Options

At a first approximation, the options market shows a similar trend as futures. Peak figures at the beginning of the year (15 billion for ether and 20 billion for bitcoin) and then a gradual decrease (to the level of 10 and 12 billion, respectively). However, this point requires clarification.

Most of the centralized trading takes place on the Derebit exchange in inverse form – i.e. is quoted in dollars, but the margin and delivery takes place in the base currency, respectively, the volume of open interest in BTC and ETH will be a more visual metric. And from this point of view, the situation is completely different – the decrease in the spot price has prompted many traders to look for a hedge in the options market. As a result, the level of interest denominated in crypto has doubled for Bitcoin and more than tripled for Ethereum. Of course, the growth of ether indicators was affected by a change in consensus and the possibility of organizing additional profitability from participation in validation and long-term storage, which naturally forces rational investors to hedge price risks.

Volatility

Three near-synchronous spikes on the yearly implied volatility chart reflect the major turmoil in the crypto market. Luna/CeDeFi/FTX are the three main culprits behind the extreme lag of cryptocurrencies from global markets. However, there is a pattern – despite the fact that bursts of volatility were higher and higher, price fluctuations in the spot market were lower and lower. So the fall of Luna led to a decline from 40,000 to 25,000 (-37.5%), celsius and 3AC sent the market from 29,000 to 20,000 (-31%), and FTX from 21,000 to 16,000 (-23%). While volatility indicators set annual records one by one. Theoretically, such a difference may indicate that the impact of negative news on the price is becoming less and indicate that the limit of the market’s fall will soon be reached.

Defi

The total amount of liquidity placed in blockchains is 39 billion, having decreased by 4 times. The Ethereum blockchain remains the undisputed leader in this indicator. The Tron blockchain came in second place, ahead of BNB Chain and Solana (whose business went downhill after the collapse of FTX). Tron took advantage of the collapse of the LUNA blockchain by offering a competitive deposit rate for stablecoins on the JustLend landing protocol.

The size of the treasure funds of the largest crypto companies has decreased from winter highs by 80%, and together with the stabilization of the Ethereum exchange rate, it froze at the level of 5 billion. Super competition in the DDAPs market constantly motivates projects to improve their own products by adding new functionality and improving the underlying algorithms. As a result, many managed to earn a significant amount. In general, there are profitable companies in many sectors – NFT trading, derivatives trading, swap exchange aggregation, gaming. The presence of leaders generating incoming financial flow is important for testing hypotheses about the state of the market, and will make it easier for startups to attract investments next year.

Trends

Defi self-regulation. The situation with Tornado Cash and the decision of many Ethereum validators to voluntarily comply with OFAC sanctions will continue. It is possible that some of the services will try to introduce some kind of KYC already at the start of work for checking for users to make sure.

Strengthening of the trend for order book trading and clob(centralized limit order book) version. Collecting quotes (centralized and decentralized) in one hybrid data provider greatly improves the efficiency of trading operations.

Defi took place. During market crises, decentralized finance services did not suffer significant losses, unlike their centralized counterparts. Smart contracts proved to be more effective than the human factor.

New large institutions. The bankruptcy of many large crypto companies, on the one hand, opened the way for new players in the market, on the other hand, it made it possible to confirm the concept of profitability of the market segment for large hedge funds and investment banks. The next wave of institutional liquidity will enter the market already with strict administrative procedures and within the framework of regulation.

Changing income models. Earnings not only from the growth of quotes, but also from the provision of services and services. If earlier the main income model involved buying cryptocurrencies and selling them after a multiple price increase, now with the launch of PoS on Ethereum, it has become possible to receive understandable passive income with understandable risks in a highly liquid market. The development of the options trading industry also allows you to receive profitability without a direct sale of a crypto asset. These factors are increasingly motivating to manage the asset’s long-term yield curve rather than speculate.

Blockchain alternative to app stores. The best way to distribute income for developers will definitely be a blockchain that is inexpensive in terms of commissions, and not an apple store with its -30% rate for each transfer

Mass nft partnership – as an example of crypto institutional B2B. The marathon of the Polygon team to provide its infrastructure for the release of NFT collections to the largest global companies has proved the demand for technology and its acceptance by corporations.

Migration of complex derivatives from traditional markets. Interest rate options, hybrid swaps, bond options – along with new mature institutional participants, the instruments they use will also come to the market.

Options dominance will rise. The trend towards growth in trading volumes and open interest will continue not only because of the attractiveness of the instrument, but also because of the arrival of new large institutional “behemoths” – professional participants in the capital market.

New models of complex real return will have an advantage over the inflation-issued attraction of capital. Attracting liquidity for the issuance of tokens for a project with colossal internal inflation will no longer be as easy as before. Participation in revenue and reward distribution based on smart contracts is a new trend that will determine the direction of movement of crypto assets between different blockchains in the next year.